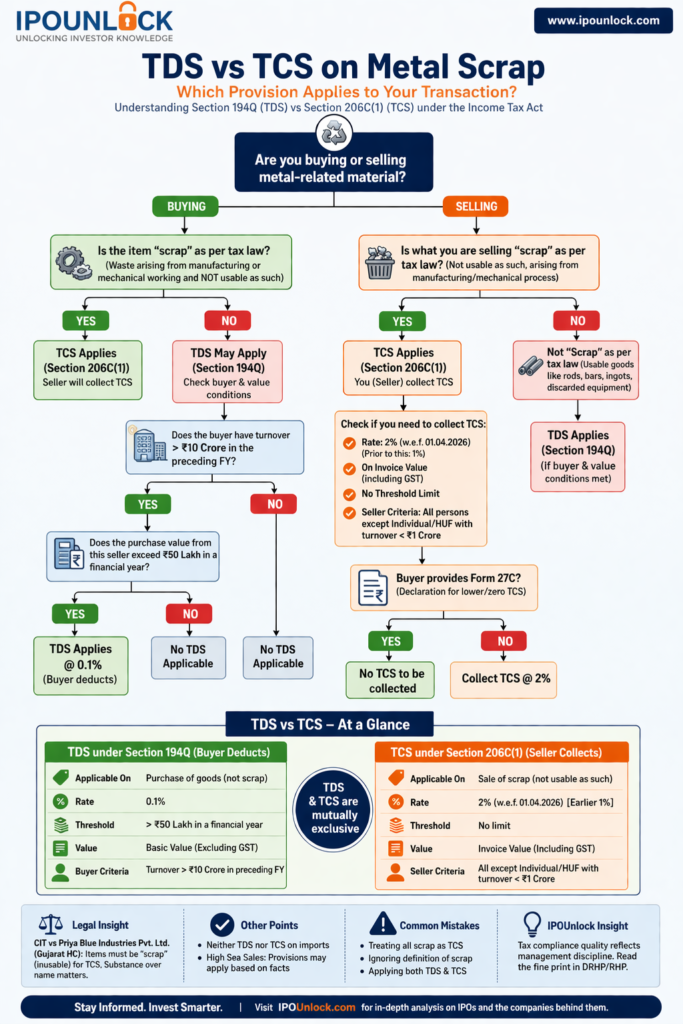

Understanding whether TDS or TCS applies on metal scrap transactions is a common challenge for businesses. The correct classification directly impacts compliance, cash flow, and tax liability. This guide explains the applicability of Section 194Q and Section 206C in a simple and practical manner.

How to Decide – TDS or TCS?

1. Basic Difference TDS VS TCS

| Particulars | TDS (Section 194Q) | TCS (Section 206C(1)) |

|---|---|---|

| Who applies? | Buyer deducts | Seller collects |

| Nature | Purchase of goods | Sale of scrap |

| Rate | 0.1% | 2% (w.e.f. 01.04.2026) |

| Threshold | ₹50 lakh | No threshold |

| Value | Excluding GST | Including GST |

2. What is “Scrap” as per Income Tax?

Scrap means:

Waste and scrap arising from manufacturing or mechanical working of materials which is not usable as such.

✔ Covered under Scrap:

- Factory metal waste

- Cutting leftovers

- Industrial unusable residue

❌ Not Considered Scrap:

- Finished goods like rods, bars, ingots

- Reusable items

- Discarded equipment (e.g., AC compressors)

👉 Key point: Name doesn’t matter—actual usability matters

3. When TCS is Applicable (Section 206C(1))

✅ Conditions:

- Sale of actual scrap

- Scrap arises from manufacturing/mechanical process

- Material is not usable as such

📌 Key Points:

- Seller collects TCS

- Rate: 2% (from 01.04.2026)

- No minimum threshold

- Applicable on invoice value (including GST)

👤 Seller Criteria:

- Applicable to all sellers except:

- Individual/HUF with turnover less than ₹1 crore in preceding year

🚫 Exception:

- If buyer furnishes Form 27C, TCS is not required

4. When TDS is Applicable (Section 194Q)

✅ Conditions:

- Goods do not qualify as scrap

- Transaction crosses threshold limits

📌 Key Points:

- Buyer deducts TDS

- Rate: 0.1%

- Applicable only if purchase exceeds ₹50 lakh in a year

- Deducted on basic value (excluding GST)

👤 Buyer Criteria:

- Buyer turnover exceeds ₹10 crore in preceding financial year

5. How to Decide – TDS or TCS?

👉 Follow this simple logic:

Step 1: Is the item “scrap” as per law?

- YES → TCS applies (206C)

- NO → Go to Step 2

Step 2: Does buyer meet threshold conditions?

- YES → TDS applies (194Q)

- NO → No TDS/TCS

6. Important Legal Position

CIT vs Priya Blue Industries Pvt. Ltd. (Gujarat HC)

- Goods from ship-breaking were sold as “scrap”

- Court held they were usable goods

- Therefore, not scrap under law

- Result: TCS not applicable

👉 Conclusion: Classification depends on nature, not terminology

7. Key Practical Points

🔹 TDS & TCS are mutually exclusive

- Only one provision applies

- No double taxation

🔹 Import Transactions

- Neither TDS nor TCS applies

🔹 High Sea Sales

- Applicability depends on transaction nature

8. Common Mistakes to Avoid

❌ Applying TCS on all scrap transactions

❌ Ignoring definition of scrap

❌ Applying both TDS and TCS

❌ Not obtaining Form 27C when eligible

9. Practical Examples

Case 1: Manufacturing Scrap

Factory sells metal waste not usable

👉 TCS @ 2% applicable

Case 2: Sale of Iron Rods as Scrap

Goods are usable

👉 TDS @ 0.1% applicable

Case 3: Small Buyer

Purchase below ₹50 lakh

👉 No TDS applicable

10. Final Conclusion

Correct tax treatment depends on classification of goods:

- ✔ True scrap (not usable) → TCS under Section 206C

- ✔ Usable goods → TDS under Section 194Q

Understanding this distinction helps avoid:

- Compliance errors

- Interest & penalties

- Tax notices

⚠️ Disclaimer

This article is intended for general informational purposes only and does not constitute professional advice. While every effort has been made to ensure accuracy, readers are advised to consult their tax advisor or chartered accountant before taking any action based on the above information. The applicability of TDS/TCS may vary depending on specific facts, nature of transaction, and updates in law.

For detailed provisions, refer to the official Income Tax Act:

👉 Income-tax Act 2025